What Is Accounting?

Accounting is the systematic process of identifying, recording, classifying, summarizing, analyzing, and reporting the financial transactions of a business or organization. It converts day-to-day transaction data into useful financial information for owners, managers, investors, lenders, tax authorities, and other users.

Accounting is often called the language of business because it communicates information about income, expenses, assets, liabilities, capital, cash flows, profit, and loss in a structured form. Transactions are generally recorded when they can be measured reliably in monetary terms.

Accounting Definition in Simple Words

In simple terms, accounting means maintaining an organized record of money received, money spent, property owned, amounts owed, and the resulting profit or loss. It helps answer questions such as:

- How much revenue did the business earn?

- What expenses did the business incur?

- Did the business make a profit or a loss?

- How much cash is available?

- What assets does the business own?

- How much does the business owe to others?

Main Steps in the Accounting Process

The accounting process begins with a financial transaction and continues until the information is presented in financial statements. Its main stages are:

- Identifying transactions: Determine which business events have a measurable financial effect.

- Recording: Enter transactions in journals and subsidiary books using appropriate supporting documents.

- Classifying: Transfer journal entries to relevant ledger accounts, such as cash, sales, purchases, rent, debtors, and creditors.

- Summarizing: Prepare account balances, a trial balance, and financial statements.

- Analyzing and interpreting: Examine financial results, trends, ratios, costs, and changes in the financial position.

- Reporting: Communicate the information to users through statements and management reports.

Recording, classifying, and summarizing form the core bookkeeping stages. Accounting has a wider scope because it also includes analysis, interpretation, reporting, planning, and decision support.

Accounting Example for a Small Business

Suppose a business owner invests $10,000 in a new store. The store then buys equipment for $3,000 in cash, purchases inventory worth $2,000 on credit, and sells goods for $1,500 in cash.

- The owner’s investment increases cash and capital by $10,000.

- The equipment purchase increases equipment and reduces cash by $3,000.

- The credit purchase increases inventory and liabilities by $2,000.

- The cash sale increases cash and sales revenue by $1,500. The cost of the goods sold is recorded separately.

Accounting records each event, assigns it to the correct accounts, and summarizes its effect on profit, cash, assets, liabilities, and owner’s equity.

Purpose of Accounting in a Business

- Accounting follows the double entry system, under which every transaction affects at least two accounts and total debits must equal total credits.

- It records financial transactions through source documents, journal entries, ledgers, and trial balances.

- It measures financial performance by determining revenue, expenses, profit, or loss for an accounting period.

- It shows the financial position of a business through information about assets, liabilities, and owner’s equity.

- It supports budgeting, cost control, pricing, planning, and other management decisions.

- It provides records needed for tax reporting, audits, statutory filings, loan applications, and communication with investors or lenders.

Advantages of Maintaining Accounting Records

- Measures profit or loss: Revenue and expenses can be compared for a specific accounting period.

- Shows financial position: A balance sheet presents the assets, liabilities, and equity of the business on a particular date.

- Tracks receivables and payables: The business can monitor amounts due from customers and amounts payable to suppliers.

- Supports cost control: Accounting records help identify production, operating, and administrative costs.

- Improves cash management: Cash receipts and payments can be monitored separately from accounting profit.

- Provides evidence: Properly maintained books and supporting documents provide a traceable record of transactions.

- Supports comparison: Current performance can be compared with budgets, earlier periods, or business targets.

Types of Accounting and Their Uses

Accounting is divided into specialized branches according to the purpose of the information and the users who need it.

- Financial accounting: Records transactions and prepares general-purpose financial statements for owners, investors, lenders, regulators, and other external users.

- Management accounting: Provides budgets, forecasts, performance reports, and decision-oriented information for internal managers.

- Cost accounting: Measures and analyzes the cost of products, services, departments, projects, or processes.

- Tax accounting: Maintains records and prepares computations required under applicable tax laws.

- Auditing: Examines accounting records, controls, and financial statements to assess whether the reported information is reliable and prepared according to relevant requirements.

- Government accounting: Records and reports the receipt, allocation, and use of public funds.

Cash, Accrual, and Hybrid Accounting Methods

An accounting method determines when revenue and expenses are recognized in the books.

- Cash system: Revenue is generally recorded when cash is received, and expenses are recorded when cash is paid.

- Accrual or mercantile system: Revenue is recorded when it is earned, and expenses are recorded when they are incurred, even when cash is received or paid later.

- Hybrid or mixed system: Certain items are recorded using the cash basis and others using the accrual basis, where the applicable accounting and tax rules permit such treatment.

For example, under cash accounting, a $1,000 credit sale may not be recognized until the customer pays. Under accrual accounting, the sale is generally recognized when the goods or services are supplied and the revenue is earned.

Bookkeeping and Accounting: Key Difference

Bookkeeping focuses mainly on the accurate and systematic recording of transactions. Accounting uses those records to classify and summarize data, prepare financial statements, evaluate performance, interpret results, and support decisions.

- Bookkeeping: Source documents, journals, ledgers, invoices, receipts, and account balances.

- Accounting: Trial balance, adjustments, financial statements, analysis, interpretation, budgeting, and reporting.

Debit and Credit in Accounting

The whole accounting process of business follows double entry system process. According to double entry, each transaction has two paths, i.e.

- Debit

- Credit

Every transaction has equal debit and credit effects, but this does not necessarily mean that one account always increases while another decreases. A transaction may increase two accounts, decrease two accounts, or increase one account while decreasing another, depending on the accounts involved.

For example, purchasing equipment for cash increases the equipment account and decreases the cash account. Purchasing inventory on credit increases inventory and also increases the amount payable to the supplier.

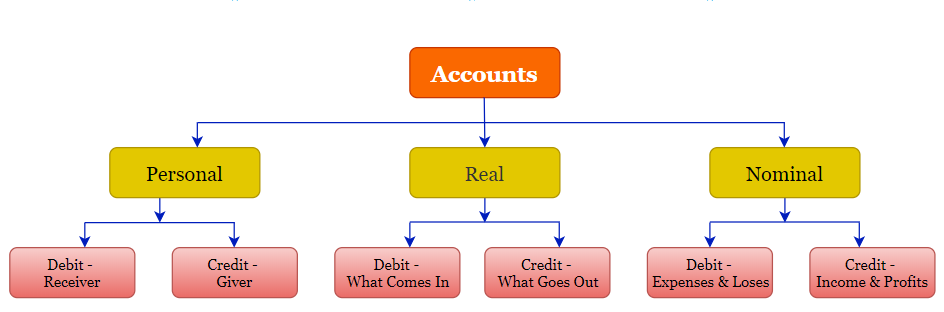

Three Types of Accounts and Traditional Debit-Credit Rules

Accounts are divided into three types under the traditional classification: personal accounts, real accounts, and nominal accounts.

1. Personal Account Rule

- Debit the receiver.

- Credit the giver.

Personal accounts relate to individuals, firms, companies, banks, institutions, and certain representative accounts.

2. Real Account Rule

- Debit what comes in.

- Credit what goes out.

Real accounts relate to assets and property, such as cash, machinery, buildings, furniture, and inventory.

3. Nominal Account Rule

- Debit all expenses and losses.

- Credit all incomes and gains.

Nominal accounts include items such as wages, rent, commission received, interest income, discounts, and losses.

Accounting Equation and Double-Entry Balance

The accounting equation represents the relationship among the resources of a business, its obligations, and the owner’s claim.

- Assets = Liabilities + Capital

- Assets – Liabilities = Capital (Owner’s Equity)

- Net Assets = Owner’s Equity.

In a company, the term owner’s equity may also include share capital, retained earnings, reserves, and other equity balances. Revenue normally increases equity, while expenses and owner withdrawals or distributions normally reduce it.

Financial Statements Prepared from Accounting Records

After transactions are recorded, classified, adjusted, and summarized, accounting information is presented through financial statements. Depending on the reporting framework and type of organization, these commonly include:

- Income statement or profit and loss account: Reports revenue, expenses, and profit or loss for a period.

- Balance sheet or statement of financial position: Reports assets, liabilities, and equity on a specific date.

- Cash flow statement: Reports cash flows from operating, investing, and financing activities.

- Statement of changes in equity: Explains changes in capital, reserves, retained earnings, and distributions.

- Notes to the accounts: Provide accounting policies, explanations, breakdowns, and other supporting details.

Who Uses Accounting Information?

- Owners and investors use it to evaluate profitability, financial stability, and returns.

- Managers use it for budgeting, pricing, cost control, planning, and performance evaluation.

- Lenders and suppliers use it to assess liquidity and the ability to repay amounts due.

- Employees may use it to understand the stability and performance of their employer.

- Tax and regulatory authorities use it to review compliance with applicable reporting and tax requirements.

- Customers and other stakeholders may use it to assess whether an organization can continue supplying products or services.

Basic Accounting Concepts for Beginners

Accounting records and reports are prepared using established concepts and assumptions. The precise requirements depend on the accounting framework and jurisdiction, but beginners should understand the following ideas:

- Business entity: Business transactions are recorded separately from the personal transactions of the owner.

- Going concern: Financial statements are generally prepared on the assumption that the business will continue operating for the foreseeable future, unless evidence indicates otherwise.

- Accounting period: Business activity is divided into reporting periods, such as a month, quarter, or financial year.

- Accrual: Income and expenses are recognized in the periods in which they are earned or incurred under accrual accounting.

- Consistency: Accounting policies should be applied consistently so that information can be compared across periods, unless a justified change is made and disclosed.

- Materiality: Information that could influence users’ decisions should be presented appropriately.

- Prudence: Estimates should be made carefully without deliberately overstating or understating financial results.

Accounting as a Course and Career

An accounting course commonly introduces journal entries, ledgers, trial balances, financial statements, cost accounting, taxation, auditing, accounting software, business law, and financial analysis. The exact syllabus depends on the qualification, institution, and country.

Accounting work may include maintaining records, reconciling accounts, preparing reports, processing payroll, reviewing internal controls, supporting tax filings, analyzing costs, preparing budgets, or examining financial statements. Job responsibilities differ across bookkeeping, financial accounting, management accounting, tax, audit, payroll, and finance roles.

Frequently Asked Questions About Accounting

What is the definition of accounting?

Accounting is the process of identifying, recording, classifying, summarizing, analyzing, and reporting financial transactions and related information.

What is accounting in one sentence?

Accounting is an organized system for recording financial activity and reporting the results and financial position of a business.

What are the three traditional types of accounts?

The three traditional types are personal accounts, real accounts, and nominal accounts. Modern accounting may also classify accounts as assets, liabilities, equity, revenue, and expenses.

What is the difference between cash and accrual accounting?

Cash accounting generally recognizes income and expenses when money is received or paid. Accrual accounting recognizes revenue when earned and expenses when incurred, even when the related cash movement occurs later.

Is accounting difficult to learn?

Accounting requires practice, accuracy, and an understanding of how transactions affect different accounts. The basic rules are manageable when learned in sequence through transaction analysis, journal entries, ledgers, trial balances, and financial statements.

Continue to read accounting tutorials that explain accounting concepts step by step with examples.