Types of Accounts in Accounting

Under the traditional approach to accounting, ledger accounts are classified as personal, real, or nominal accounts. This classification helps determine the correct debit and credit treatment for each transaction.

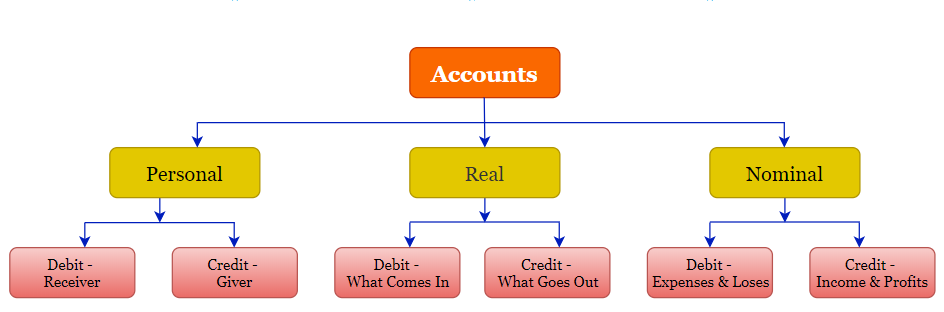

The three traditional types of accounts are:

Personal, Real, and Nominal Accounts at a Glance

| Account type | What it represents | Debit rule | Credit rule |

|---|---|---|---|

| Personal account | Individuals, companies, firms, banks, and organizations | Debit the receiver | Credit the giver |

| Real account | Tangible and intangible assets | Debit what comes in | Credit what goes out |

| Nominal account | Expenses, losses, incomes, and gains | Debit all expenses and losses | Credit all incomes and gains |

Personal Accounts in Accounting

A personal account represents a person or an entity with which the business has transactions. It may relate to an individual, company, partnership firm, bank, government body, or another organization.

Examples of personal accounts include a customer’s account, supplier’s account, bank account, ABC Limited A/c, and Tutorial Kart A/c.

Types of Personal Accounts

- Natural personal accounts: Accounts of individual people, such as John A/c or Priya A/c.

- Artificial personal accounts: Accounts of companies, banks, firms, institutions, and organizations.

- Representative personal accounts: Accounts that represent a person or group of persons, such as Outstanding Salary A/c or Prepaid Insurance A/c.

Personal Account Rule

- Debit the receiver

- Credit the giver

When a person or entity receives value from the business, that personal account is debited. When a person or entity gives value to the business, that personal account is credited.

Example: Tutorial Kart paid $5,000 to ABC Limited by check. ABC Limited receives the payment, so ABC Limited A/c is debited. The payment leaves the bank account, so Bank A/c is credited.

| Date | Particulars | Debit ($) | Credit ($) | Rule applied |

|---|---|---|---|---|

| 20-Jun-19 | ABC Limited A/c Dr. | 5,000 | Debit the receiver | |

| 20-Jun-19 | To Bank A/c | 5,000 | Credit what goes out |

The entry combines the personal account rule for ABC Limited with the real account rule for the bank balance.

Real Accounts in Accounting

A real account represents an asset owned or controlled by the business. Real accounts record the movement and balance of assets and generally continue from one accounting period to the next.

Tangible and Intangible Real Accounts

- Tangible real accounts: Cash, buildings, furniture, machinery, inventory, land, and equipment.

- Intangible real accounts: Goodwill, patents, copyrights, trademarks, and software rights.

Real Account Rule

- Debit what comes in

- Credit what goes out

When an asset enters the business, its account is debited. When an asset leaves the business, its account is credited.

Example: Furniture was purchased for $790 in cash on June 10, 2019. Furniture comes into the business, while cash goes out.

| Date | Particulars | Debit ($) | Credit ($) | Rule applied |

|---|---|---|---|---|

| 10-Jun-19 | Furniture A/c Dr. | 790 | Debit what comes in | |

| 10-Jun-19 | To Cash A/c | 790 | Credit what goes out |

Both accounts in this transaction are real accounts. The asset received is debited, and the asset paid out is credited.

Nominal Accounts in Accounting

Nominal accounts record expenses, losses, incomes, and gains for a particular accounting period. They are temporary accounts because their balances are transferred to the profit and loss account at the end of the period rather than carried forward as continuing asset or liability balances.

Examples of nominal accounts include rent, salary, wages, purchases, sales, commission received, interest received, depreciation, and loss on sale of an asset.

Nominal Account Rule

- Debit all expenses and losses

- Credit all incomes and gains

Expenses and losses reduce the profit of the business and are debited. Incomes and gains increase profit and are credited.

Example: Goods were purchased for $2,000 in cash. Under the traditional approach, Purchases A/c is treated as a nominal account and is debited. Cash is a real account and is credited because cash goes out of the business.

| Date | Particulars | Debit ($) | Credit ($) | Rule applied |

|---|---|---|---|---|

| 10-Jun-19 | Purchases A/c Dr. | 2,000 | Debit expenses or purchases | |

| 10-Jun-19 | To Cash A/c | 2,000 | Credit what goes out |

Examples of Personal, Real, and Nominal Accounts

| Account | Account type | Reason |

|---|---|---|

| Customer A/c | Personal | Represents an individual or business that owes money |

| Supplier A/c | Personal | Represents a person or organization supplying goods or services |

| Outstanding Salary A/c | Representative personal | Represents salary payable to employees |

| Cash A/c | Real | Represents a tangible business asset |

| Machinery A/c | Real | Represents a tangible fixed asset |

| Goodwill A/c | Real | Represents an intangible asset |

| Rent A/c | Nominal | Represents an expense |

| Commission Received A/c | Nominal | Represents income |

| Loss on Sale of Asset A/c | Nominal | Represents a loss |

How to Identify the Account Type in a Transaction

- Identify every account affected by the transaction.

- Ask whether the account represents a person or organization, an asset, or an expense, income, gain, or loss.

- Classify it as personal, real, or nominal.

- Apply the debit and credit rule for that account type.

- Check that the total debit equals the total credit.

For example, when rent is paid in cash, Rent A/c is nominal because it is an expense, and Cash A/c is real because it is an asset. Rent is debited, and Cash is credited.

Traditional Account Types and Modern Account Classification

Personal, real, and nominal accounts belong to the traditional classification system. Modern accounting systems commonly group accounts as assets, liabilities, equity, revenue, and expenses. The terminology differs, but both methods should produce the same balanced journal entry when applied correctly.

| Traditional classification | Common modern classification | Examples |

|---|---|---|

| Personal account | Asset or liability | Customer receivable, supplier payable, bank loan |

| Real account | Asset | Cash, furniture, machinery, goodwill |

| Nominal account | Expense or revenue | Rent, salary, sales, commission income |

Personal, Real, and Nominal Account Review Checklist

- Confirm that personal accounts represent identifiable people, firms, banks, or organizations.

- Check whether a real account is a tangible or intangible asset.

- Verify that nominal accounts relate only to expenses, losses, incomes, or gains.

- Apply the correct golden rule to each account in the transaction.

- Ensure that example amounts and debit and credit totals match.

Types of Accounts FAQs

What are the three traditional types of accounts?

The three traditional types are personal accounts, real accounts, and nominal accounts. Personal accounts represent persons and entities, real accounts represent assets, and nominal accounts represent expenses, losses, incomes, and gains.

What is the rule for a personal account?

The rule for a personal account is to debit the receiver and credit the giver.

Is cash a real account?

Yes. Cash is a tangible asset and is therefore classified as a real account under the traditional system.

Is goodwill a real or nominal account?

Goodwill is an intangible real account because it represents an identifiable business asset rather than an expense or income for a single period.

What is the difference between a real account and a nominal account?

A real account represents an asset whose balance generally carries forward to the next accounting period. A nominal account records an expense, loss, income, or gain for the current period and is closed at the end of that period.